Si riapre la querelle sulla decarbonizzazione europea e gli incentivi sulla “trasformazione verde”

(Rinnovabili.it) – Il ministro dell’energia polacco Krzysztof Tchorzewski ha dichiarato che l’obiettivo europeo delle zero emissioni entro il 2050 è pura fantasia. A riportarne le parole è l’agenzia di stampa polacca Polska Agencja Prasowa, che riaccende così la miccia di una querelle tutta europea sulla strategia di decarbonizzazione.

Secondo PAP, Tchorzewski ha dichiarato che la Polonia dovrebbe affrontare dei costi pari a 700-900 miliardi di euro per raggiungere un’economia netta a emissioni zero. A detta del ministro, però, questa cifra (ovviamente distribuita su anni) potrebbe essere ridotta predisponendo degli incentivi economici, a suo parere necessari affinché la Polonia non subisca delle gravi perdite in termini economici e possa mantenersi al passo con gli altri Stati membri.

Una posizione simile era già stata espressa durante il Consiglio Europeo di giugno scorso, quando la possibilità di una strategia condivisa di decarbonizzazione a lungo termine aveva fatto esplodere il conflitto tra Stati occidentali e orientali in Europa. In quell’occasione, la Polonia si era opposta alla richiesta del cancelliere tedesco Angela Merkel affinché l’UE raggiungesse l’obiettivo delle zero emissioni entro il 2050. Anche in quel frangente, la questione sollevata dal presidente del Consiglio dei ministri polacco, Mateusz Morawiecki, riguardava la necessità di predisporre dei pacchetti di compensazioni per gli Stati membri.

La sua posizione era stata appoggiata dal primo ministro ceco, Andrej Babis, il quale aveva inoltre espresso preoccupazione per la competitività europea in ambito economico, specie in assenza di comparabili impegni sulla decarbonizzazione da parte di altri paesi, compresa la Cina. Anche il presidente ungherese Viktor Orban aveva appoggiato l’opinione del presidente del Consiglio polacco in merito alla necessità di regolamentare degli incentivi per la “trasformazione verde”.

Per tale ragione, il ministro dell’energia polacco esclude che il paese possa raggiungere l’obiettivo di aumentare la percentuale di energie rinnovabili nel mix energetico al 21% entro il 2030.

Market evolution is driving change in how companies strategically manage their energy. This changing landscape opens opportunities for businesses to modify their energy consumption mix, with potential cost savings as a result. Increases in data-driven technology also help companies better understand their real-time, interval energy consumption and demand, which can provide the visibility required to curtail usage when prices spike or better negotiate contracts according to individual site consumption and demand patterns.

Strategic energy management can result in significant cost savings. But respondents to our recent corporate energy and sustainability research report indicate strategic sourcing as a top savings opportunity only 29% of the time. This is unfortunate, as businesses with strategic sourcing initiatives are also more likely to explore innovative technologies and invest in other complementary technologies such as combined heat and power, battery storage and renewables.

There’s also increasing complexity in energy sourcing as markets begin to diversify their generation mix. Renewable technologies are now some of the most affordable electricity sources in the world and the result is higher renewable penetration than ever before.

The upside to this market evolution is that cloud-service, colocation, and data center companies have an immense opportunity to save money and balance their generation sources. But this opportunity also comes with a downside: the need to manage energy and risk in a more nuanced and strategic way.

Change is Afoot: How the Market is Evolving

Market evolution introduces new considerations for technology companies to weigh as part of their overall procurement strategy. No longer is renewable energy an add-on for only the most progressive and environmentally-minded organizations. Renewables have become a key business strategy for many companies in the cloud-service and data center space, an industry that consistently leads the way in annual procurement of renewables via long-term corporate power purchase agreements (PPAs).

Data center and cloud-service providers are consistently ranked among the largest users of renewable energy. In 2019, Equinix, Digital Realty, Salesforce and Iron Mountain are listed in the U.S. EPA’s Green Power Partnership National Top 100.

Some evidence of the changes being driven by market evolution:

Renewables are becoming central to business. Corporate investment in renewable energy continues at a rapid pace; 2018 was a record-breaking year with 13.4 GW of renewable energy contracts executed by corporations, and 2019 is predicted to follow this path. More than 150 corporations globally have committed to 100% renewable energy, with cloud-service and data companies being among some of the founding members of the RE100 initiative.

Energy buyers are becoming more sophisticated. At the most basic level, energy buyers that used to simply accept the traditional grid electricity mix and pricing are getting more strategic about how, when and what type of energy they use. Organizations that buy energy attribute certificates (EACs) are now exploring contractual instruments in some of the most challenging global markets to advance development and meet procurement or carbon-reduction goals. Companies executing long-term PPAs are testing new collaborative solutions, such as aggregated buying, and innovative contract terms and structures like cap and collar or Microsoft’s VFA. Exploration and adoption of microgrids is on the rise. And some companies are exploring all these options—and more.

To meet diverse goals, companies need cross-silo collaboration. It’s becoming imperative for companies to align on energy activities across traditional procurement, renewables, efficiency and sustainability, with data as the major intersection. Some companies go beyond simply aligning activities and sharing data; the most forward-thinking organizations expect to fully integrate sourcing and reporting for traditional energy and renewable energy into an active energy management strategy.

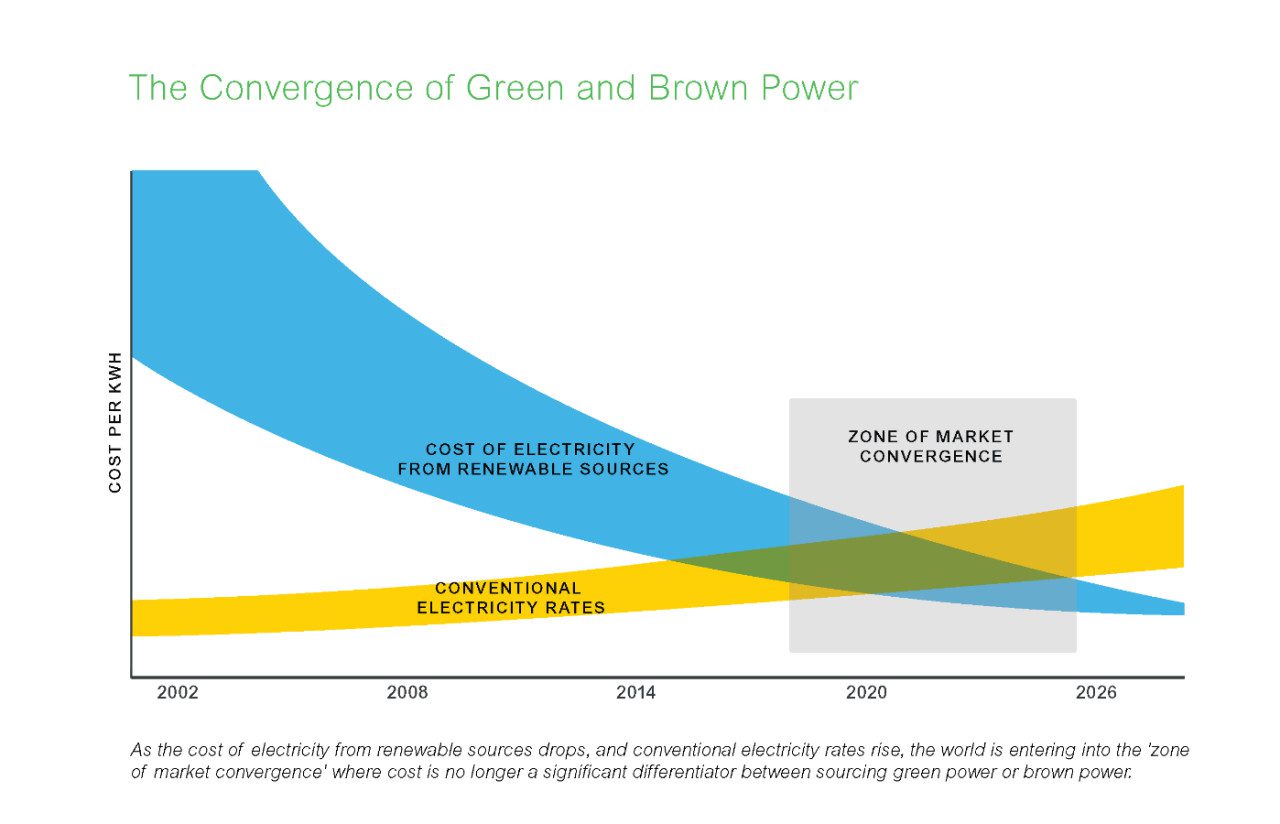

The Convergence of Green & Brown Power Drives Evolution

Emerging price parity of green power (such as wind and solar) and brown power (power traditionally supplied by the grid) is a cornerstone of the evolution of the energy market. The cost of wind and solar power have been on a swift decline for the past decade, bolstered by subsidization and increasing efficiencies in both technology and scale. As a result, renewable penetration on the grid has now reached roughly 33% globally, with increasing adoption forecast. This growth means that, alongside traditional brown power options for electricity, green power is now emerging as a more cost-effective choice. It also means that there are more suppliers in the market than ever before, and organizations in deregulated retail regions can now potentially evaluate green and brown power procurement on a level playing field.

Source: Schneider Electric – based on indicative, not actual, market prices.

How is convergence likely to impact your business?

Green power will become more accessible. If you haven’t already, you will begin to see increasing access to green power options around the world. The low price—and increasing demand for fossil-free generation—means that there has never been a greater opportunity to adopt renewables.

Adopting green power will be more cost-effective. Green power options are increasingly affordable, and for those solutions that may require a CapEx investment (such as an owned, onsite solar system), energy efficiency and energy-as-a-service solutions are potential avenues towards financial enablement.

And companies will find synergies by breaking down organizational silos. The resulting combination of strategic sourcing, renewables procurement and efficiency form the basis for a more sophisticated integrated and cost-saving energy solution. Organizations are more likely to begin purchasing bundled services from electricity providers than can address their energy needs holistically as a result.

But buyers must be aware when new opportunities emerge. As existing energy service providers take more innovative approaches to their services, and new providers enter the market hoping to capitalize on this growing need, organizations must be critical of any service offer, and ensure that it provides the greatest benefit with the lowest exposure. For instance, it can be attractive to companies to accept green power solutions provided by their traditional power supplier to streamline complexity. However, these solutions should be assessed alongside other available options in the market, to ensure you do not lock into a deal that exposes you as a buyer to unnecessary risk.

Navigate the Market Convergence

Fundamental changes in the generation mix are driving market evolution and making it more complex than ever for technology companies to purchase energy. An independent advisor like Schneider Electric Energy & Sustainability Services can help you evaluate your choices as the market converges to ensure you get the best products at the best price for your needs.

To learn more about how to navigate market convergence, the associated opportunities and challenges and how your company can prepare, watch our recent webinar with Smart Energy Decisions.

Cogesa SpA apre un avviso per l’affidamento dei lavori di allestimento del lotto III della discarica per rifiuti non pericolosi e lavori di realizzazione dei pozzi di estrazione del biogas sul lotto II. La gara si terrà il 14/10/19. Importo: 980.338 euro Scadenza: 14 ottobre 2019 Il bando

Lamezia Terme (CZ) appalta un intervento di efficientamento energetico di un comparto della pubblica illuminazione nel territorio comunale. Importo: 232.429 euro Scadenza: 17 ottobre 2019 Il bando

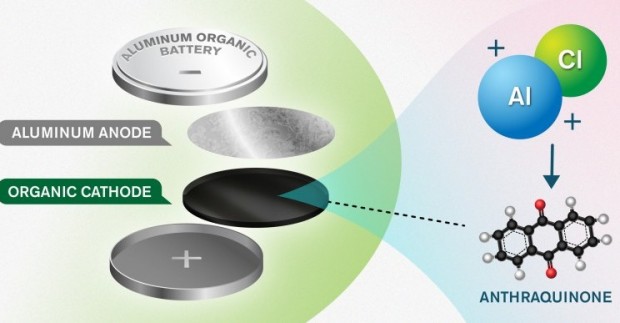

Credit: Yen Strandqvist / Chalmers University of Technology

Una molecola organica sostituisce la grafite nelle nuove batterie a ioni alluminio

(Rinnovabili.it) – Le batterie ricaricabili a ioni alluminio rappresentano oggi uno dei più promettenti sostituti della tradizionale tecnologia a base di litio. A basso costo e bassa infiammabilità,questi dispositivi di accumulo offrono un’alta capacità volumetrica: l’energia immagazzinata per volume nelle batterie a ioni alluminio è superiore a quella delle altre batterie metalliche (fino a 4 volte quella del litio), con la possibilità dunque di avere unità con dimensioni ridotte ma elevata capacità.

L’uso di questa tecnologia potrebbe dunque comportare numerosi vantaggi, tra cui un’alta densità di energia teorica e, visto l’elemento principale, ancheuna produzione economica e una filiera del riciclo già consolidato (leggi anche Batterie all’alluminio: più economiche e sostenibili).

I precedenti progetti in questo campo avevano usato l’alluminio come anodo (l’elettrodo negativo) e la grafite come il catodo (l’elettrodo positivo). Ma la grafite fornisce un contenuto energetico troppo basso per creare celle con prestazioni sufficienti per essere utili a livello commerciale. Per risolvere il problema un gruppo di ricercatori internazionali ha messo a punto un nuovo concept. Parliamo del lavoro svolto dagli scienziati della Chalmers University of Technology della Svezia, e dell’Istituto Nazionale di Chimica in Slovenia. “I costi dei materiali e gli impatti ambientali del nostro prototipo sono molto più bassi di quelli attuali, rendendo la tecnologia fattibile per l’uso su larga scala, a livello di impianti solari ed eolici”, spiega Patrik Johansson, professore presso il Dipartimento di Fisica di Chalmers. “Inoltre, possiede una densità energetica doppia rispetto all’attuale stato dell’arte per le batterie in alluminio”.

Il lavoro, presentato da Patrik Johansson e Chalmers, insieme a un gruppo di ricerca guidato da Robert Dominko, ha sostituito a livello del catodo la grafite con un materiale organico nanostrutturato a base di antrachinone. Il vantaggio di questo molecola è che consente la conservazione dei portatori di carica positivi dall’elettrolita, portando ad una maggiore densità di energia nella batteria.

“Poiché il nuovo materiale catodico consente di utilizzare un supporto di carica più appropriato, le batterie possono sfruttare meglio il potenziale dell’alluminio. Ora stiamo proseguendo il lavoro cercando un elettrolita ancora migliore. La versione attuale contiene cloro: voglio liberarcene”, afferma la ricercatrice di Chalmers Niklas Lindahl, che studia i meccanismi interni che regolano l’accumulo di energia. Il lavoro è stato pubblicato su Energy Storage Materials(testo in inglese)

This website uses cookies to improve your experience. We'll assume you're ok with this, but you can opt-out if you wish. Cookie settingsACCEPT

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.